Global Mortgage Rates Comparison 2025

Comprehensive analysis of mortgage rates across 61 countries worldwide

Executive Summary

Global Landscape

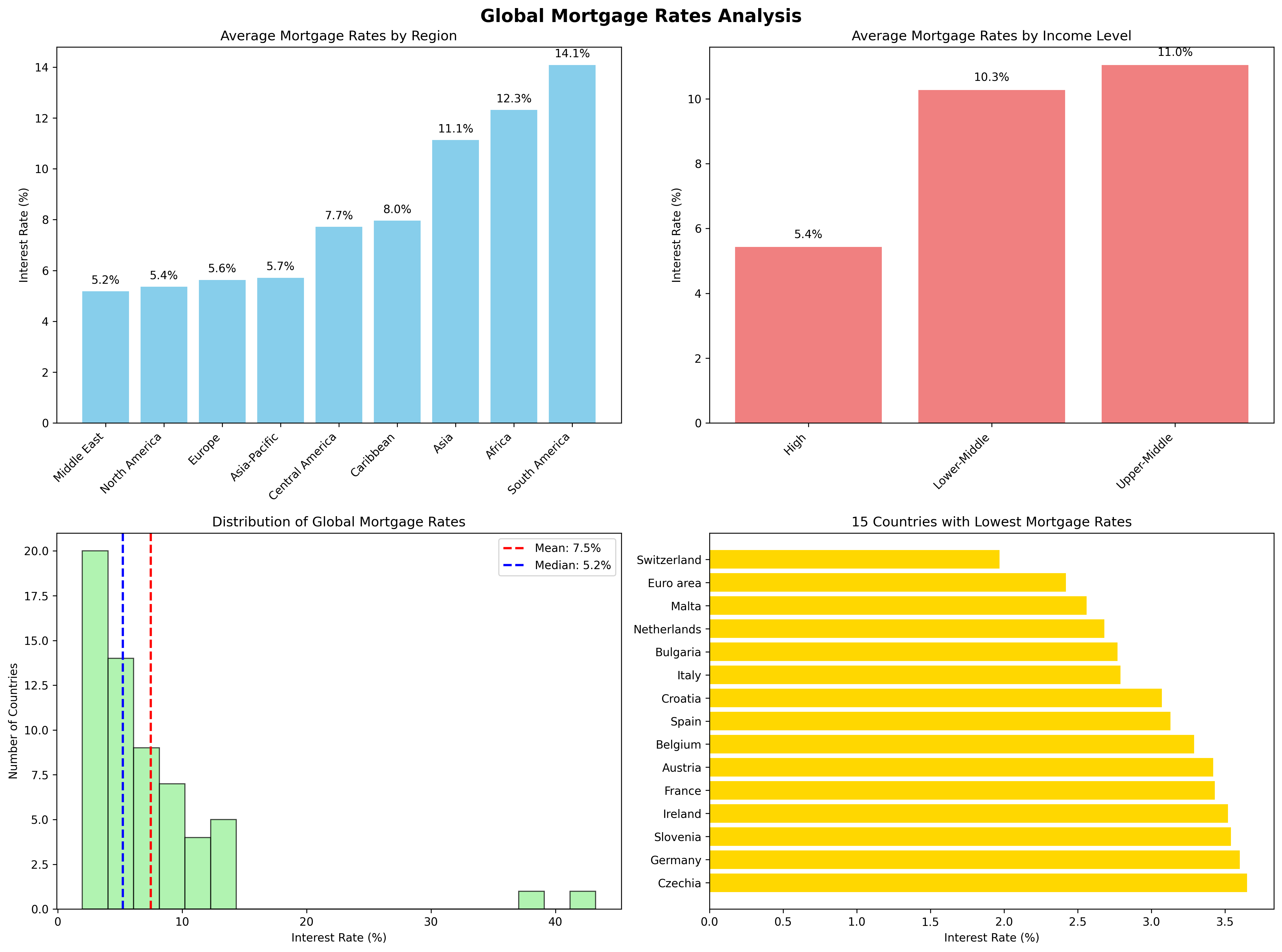

Mortgage rates vary dramatically worldwide, from Switzerland's 1.97% to Turkey's 43.23%, reflecting diverse economic conditions and monetary policies.

Regional Patterns

Europe leads with the lowest average rates (5.63%), while South America shows the highest variability due to economic instability.

Economic Correlation

High-income countries average 5.43% rates, while upper-middle income countries average 11.05%, showing clear development correlation.

Key Findings

European Dominance

9 out of 10 countries with the lowest mortgage rates are European, led by Switzerland at 1.97%.

Hyperinflation Impact

Countries experiencing economic instability show extreme rates: Turkey (43.23%) and Argentina (37.84%).

Development Gap

A 5.62 percentage point difference exists between high-income and upper-middle income countries.

Regional Analysis

Regional Averages

Country-by-Country Data

| Rank | Country | Current Rate (%) | Region | Income Level |

|---|

Factors Affecting Mortgage Rates

Inflation

Lenders adjust rates to maintain real returns above inflation. Countries with high inflation typically see higher mortgage rates to compensate for currency devaluation.

Central Bank Policy

Monetary policy decisions significantly impact mortgage rates. Central banks influence rates through policy rate adjustments and money supply management.

Bond Markets

Mortgage-backed securities compete with government bonds. The 10-year Treasury yield serves as a key benchmark for mortgage rate pricing.

Housing Market

Supply and demand dynamics in housing markets directly affect mortgage demand and pricing. Constrained supply amplifies rate impacts.

Economic Stability

Political and economic stability correlate with lower rates. Countries with stable institutions typically offer more competitive mortgage terms.

Currency Risk

Exchange rate volatility affects foreign-currency mortgages. Stronger currencies typically correlate with lower domestic mortgage rates.

Market Insights & Implications

For International Investors

Significant geographic arbitrage opportunities exist for international property investment. European markets offer the most favorable financing conditions, while emerging markets present higher-risk, higher-return scenarios. Currency hedging becomes crucial when investing across borders due to exchange rate volatility.

For Homebuyers

Location significantly impacts borrowing costs. Homebuyers in developed economies benefit from lower rates and more stable lending conditions. Those in emerging markets face higher costs but may benefit from rapid property appreciation in growing economies.

For Policymakers

Mortgage market characteristics significantly influence monetary policy transmission. Countries with higher fixed-rate mortgage prevalence experience delayed but potentially stronger policy effects. Housing supply constraints amplify monetary policy impacts on both prices and economic activity.

Data Sources & Methodology

This analysis is based on the most recent available data from authoritative sources including:

- The Global Economy - Central bank and national statistical office data

- Global Property Guide - International mortgage market data with 20-year historical perspective

- International Monetary Fund (IMF) - Housing market research and monetary policy analysis

- Investopedia - Financial market analysis and rate factor research

Data represents the latest available mortgage rates for each country as of 2024-2025, sourced from central banks and national statistical offices. Rates reflect local currency lending to residents and may vary based on loan terms, borrower qualifications, and market conditions.